Economist overboard!

Its been a weird couple of weeks for Paul Krugman. First he popped up on CNN to speculate that the threat of an alien invasion of earth might be good for the economy. Lots of scope for Keynesian stimulus spending on ray guns you see.

Then he was forced to take to his blog to deny that that following the recent earthquake on the eastern seaboard of the United States he had said

“People on twitter might be joking, but in all seriousness, we would see a bigger boost in spending and hence economic growth if the earthquake had done more damage”

The fact that many of the comments on that post on the now deleted Google + page of the fake Krugman were from Keynesians defending the statement rather undermines Krugman’s indignation when he bridled at being called a cheerleader for destruction.

But his denial of the earthquake comments contained yet another far out statement from the whack economist

“Just to be clear: World War II was expansionary because it led to a large increase in public spending”

Lets leave until another day the argument that the act of destroying large sections of the planet’s labour force and capital stock can in any conceivable way be said to exercise an “expansionary” effect on an economy you have to wonder where exactly Krugman has been for the past decade. And what has he been doing there?

We have had, along with the Americans, two foreign wars. Krugman’s fellow Keynesian Joseph Stiglitz estimated the cost of just the war in Iraq at $3 trillion. How’s that for stimulus?

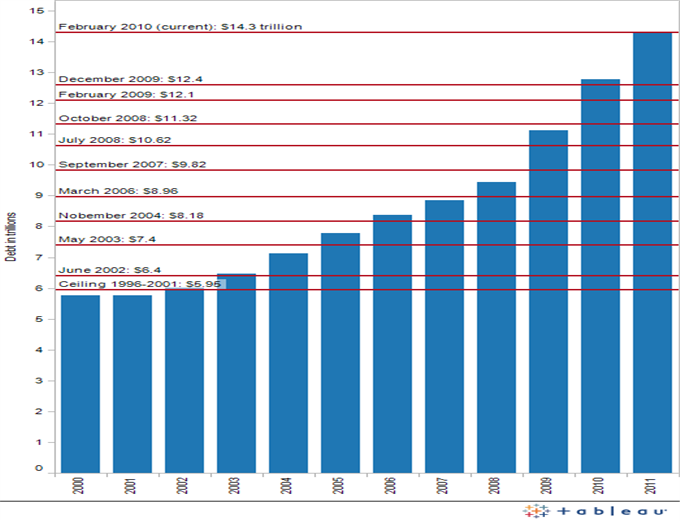

The Federal debt ceiling was raised from just under $6 trillion in 2001 to nearly $10 trillion on the eve of the Lehman Brothers collapse in 2008. A massive stimulus and the economy still tanked.

Federal debt ceiling

So Krugman’s prescription for an ailing economy is a massive dollop of stimulus spending. That’s it. The same thing, in other words, that was being done to the economy as it hit the wall in 2007-2008. Maybe Krugman should stick to Space Invaders.